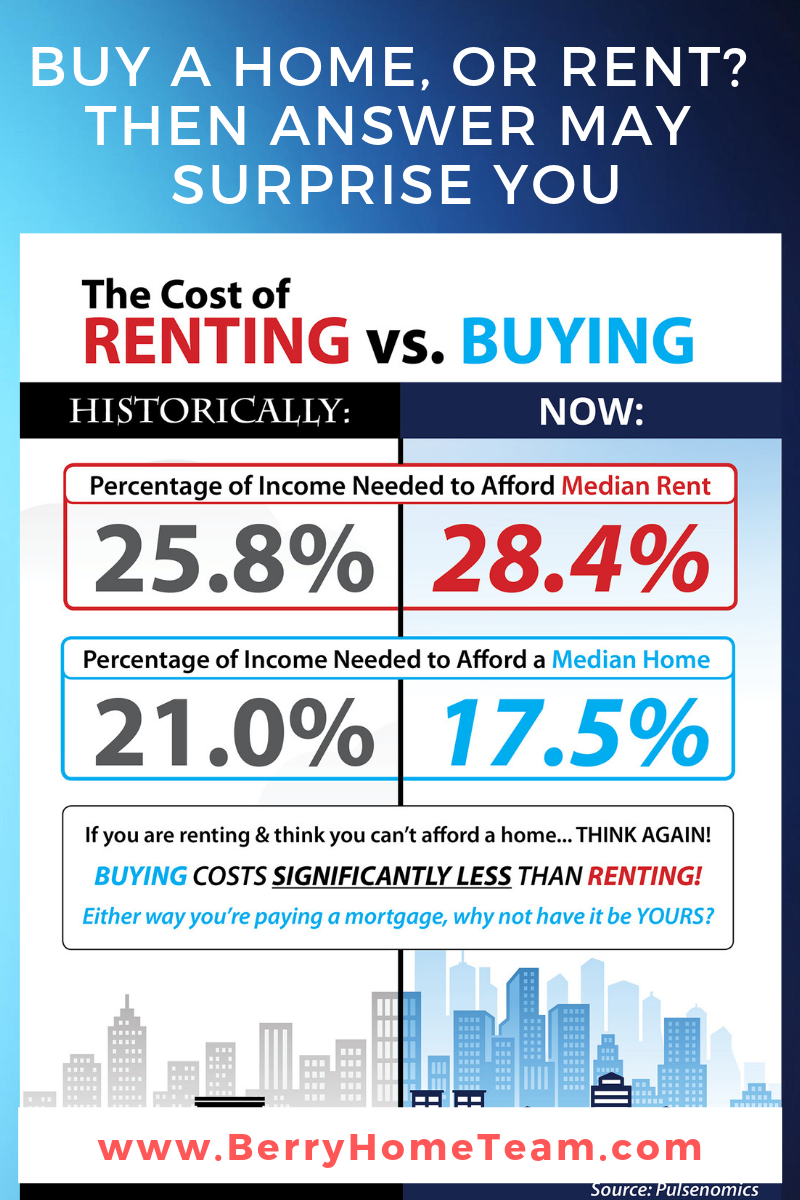

Historically, the choice between renting or buying a home has been a tough decision.

If you look at the percentage (%) needed to rent a median-priced home today (28.4%) vs. the percentage (%) needed to buy a median-priced home (17.5%), the choice becomes clear and obvious.

Obviously, every real estate market is different, but before you renew your lease again, let us help you find out if you can put your housing costs to work for you by buying a home this year instead.

We can also help anyone who is considering purchasing a home to rent out to tenants, and letting them help pay your mortgage for you.

Renting vs. buying a home: Calculating the costs

The first consideration in the rent vs. buy decision is often how much each will cost. If you rent a home, your monthly costs are generally fixed for the term of the lease. Your monthly rent may or may not include utilities such as electric, gas, cable or internet. Most leases require the first month’s rent, last month’s rent and a security deposit equal to one month’s rent in advance. For an apartment that costs $1,000 per month, you’d typically need $3,000 up front. Keep in mind, though, that landlords can in most places increase the rent as much as they like when the lease ends or sell the property you’re renting, so you may have to move a few times.

The good news: When you’re a tenant, your landlord is generally responsible for fixing any issues with the property, whether it’s a leaky roof, a cranky furnace or a burst pipe.

How much house can I afford?

When buying a home, most mortgage lenders require a down payment between 3 percent and 20 percent of the home’s price. Some loans may have a lower threshold, but down payments below 20 percent will mean paying for private mortgage insurance, or PMI, which is an additional monthly expense. You’ll also pay closing costs, which average 2 percent to 4 percent of the home’s price. A

mortgage calculator can give you a rough estimate of your monthly payments, including your interest and principal outlays and other expenses such as property taxes, homeowners insurance and, in some cases, homeowners association dues. A housing affordability calculator can help you determine how much house you can afford. But our financial responsibility doesn’t end with your monthly mortgage payment. You’ll also need to pay for utilities, maintenance and repairs, whether it’s a few bucks to fix a leaky faucet or thousands to replace a roof.

Reasons to buy a home

Buying a home can be a great investment. If home prices in your area have been rising, buying now can help you stay in a neighborhood that you might otherwise be priced out of in a few years. And even if you don’t end up staying long term, a sharp rise in local property values could mean a sizable profit when you sell. Some indications that buying may be right for you:

You plan to stay in the same place for more than a few years.

You’d be willing to rent out part or all of your home, should your plans or finances change.

You’re eligible for a prime-rate mortgage, with payments you can afford.

You’re willing to put some “sweat equity” into a fixer-upper, allowing you to buy something more affordable. You can increase the home’s value with improvements over time.

Reasons to rent a home

Though owning your own home can offer a sense of security, homeownership has its drawbacks — remember the roof replacement? Getting out of a lease is also much less of an ordeal than selling a house, so if you’re not sure where you’ll be next year, renting can save you some costly headaches. Some indications that renting may be right for you:

You aren’t sure how long you’ll be in the home because of work, changing family circumstances or other reasons.

You won’t be able to afford — or don’t want to bother with — the maintenance or repairs a house may need.

Your finances are variable or likely to change soon, potentially making it difficult to keep up with mortgage payments.